Why biophysical economics matters

IN SHORT:

Almost a decade after the onset of the financial and economic crisis, the global economy remains weak and the hoped-for ‘recovery’ elusive. The economic policies conducted in the last few years have largely failed to re-start the growth engine, and no return to pre-crisis growth rates is in sight; on the contrary, lower growth seems to have become the world’s new reality. This global dearth of economic growth is causing significant disruption and generating major challenges in a world that had previously become accustomed to rapid expansion. In particular, it is feeding a seemingly unstoppable rise of economic and political instability in developed as well as emerging economies. For policy makers and for civil society, there is therefore no more important and pressing need than to understand the causes and consequences of this ‘great deceleration’, as well as the policy options that may – or may not – be available to address them. Biophysical economics provides the theoretical and practical basis to meet this need.

IN MORE DETAIL:

Almost a decade after the onset of the global financial and economic crisis that erupted in 2007-2008, the global economy remains weak and the hoped-for ‘recovery’ elusive:

- In the U.S., the post-recession rebound has been the weakest on record and the economy is still struggling to reach and maintain ‘escape velocity’.

- Japan, which has been plagued with low growth for over two decades, is so far failing to revive its stalled economy despite unprecedented monetary and fiscal stimulus measures.

- In China, growth is faltering after three decades of breakneck economic expansion.

- Most other emerging economies, meanwhile, seem to have hit a wall, having either exhausted their catch-up growth models or failed to diversify from commodity exports.

- Europe, where the damages of the financial crisis have been compounded by the design flaws of the continent’s monetary union, is still struggling to extract itself from a state of prolonged stagnation.

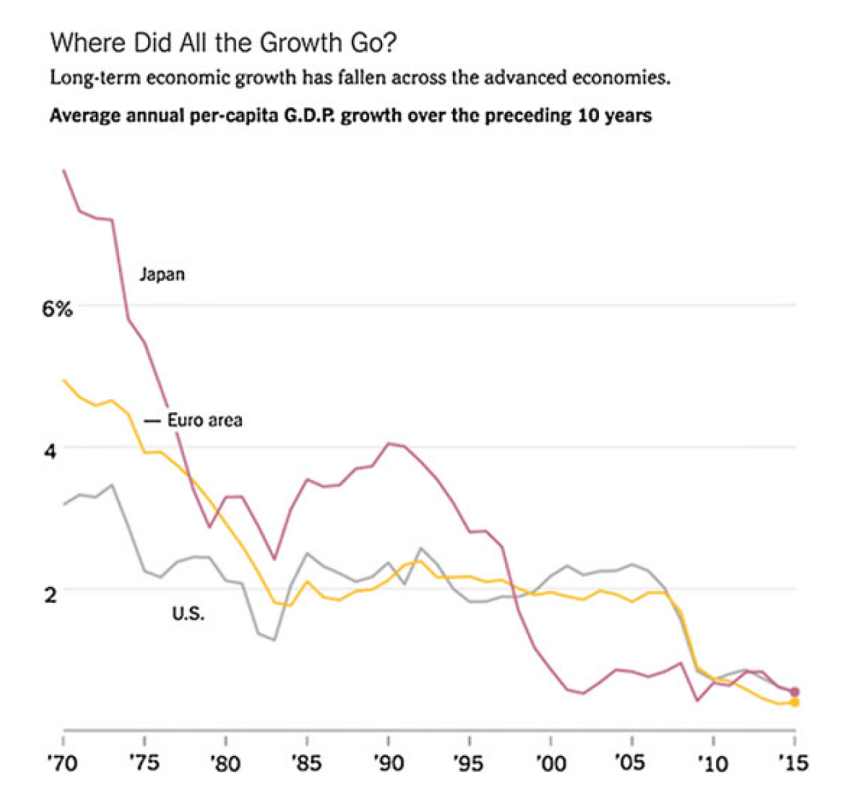

Figure 1: GDP growth rates of selected OECD entities. Each point reflects average growth over preceding 10 years. Source: Charles A.S. Hall, based on World Bank Data

According to most estimates, global real economic growth (i.e. adjusted for inflation) now barely reaches 3% a year, well below pre-crisis levels, and is trending even lower. Over the last few years, international organizations such as the World Bank (WB), the International Monetary Fund (IMF), or the Organisation for Economic Cooperation and Development (OECD) have made a habit of regularly revising their global growth forecasts down. The economic policies conducted in the last few years – including unprecedented monetary stimulus by the world’s main central banks in the form of ultra-low interest and ‘Quantitative Easing‘ (QE) – have thus largely failed to trigger the economic recovery that was hoped for and expected after the ‘Great Recession’. No return to pre-crisis growth rates seems to be in sight; on the contrary, lower growth seems to have become the world’s new reality.

This global dearth of economic growth is causing significant disruption and generating major challenges in a world that had previously become accustomed to rapid expansion, and where economic growth – as measured by the increase of Gross Domestic Product (GDP) – has come to be considered as the ‘normal’ and almost ‘natural’ state of things, i.e. where growing output, incomes and profits is viewed as a sign of economic health, whereas non-growth is perceived as a sign of economic and societal disease and distress.

In the Western world in particular, businesses assume that their revenues and profits ought to grow, consumers that their purchasing power and living standards ought to go up, governments that their tax revenues will naturally rise over time and make it possible to fund their policies and spending plans. Lenders and investors assume that borrowers will be able to repay their debts with interest, and businesses to pay dividends. All make their spending and investment decisions, as well as related long-term financial commitments, on the basis of the widely shared assumption that the economy will grow and that they will be able to get their share of an expanding pie. Voters, in turn, assume that political leaders will maximize economic growth and use its proceeds to constantly increase societal welfare.

The assumption of – and need for – continuous and significant growth has in fact become so much embedded in the world’s established economic, political and social order, that growth has become a key requirement for this order to keep functioning and to remain stable. A prolonged period of low growth would undermine this order in several and mutually reinforcing ways, as it would be likely to:

- hamper the rise of living standards as economic expansion fails to keep up with population growth;

- exacerbate income and wealth concentration and inequality in developed and developing economies, as the process of capital accumulation increasingly takes place in a context where there is no more ‘rising tide to lift all boats’;

- increase financial instability, volatility and distress as revenues, incomes and profits fail to keep up with expectations;

- make it increasingly difficult to maintain fiscal sustainability as the tax base grows more slowly than planned while spending needs keep mounting;

- increase social tensions and political polarization in developed as well as developing economies, leading to popular discontent, the rise of populist or authoritarian movements, social unrest and even violence in some cases;

- increase the risk of political/geopolitical dislocation or fragmentation, potentially leading to conflicts between competing groups, nations or blocs for scarcer growth proceeds, as well as to significant displacements of population.

To some extent, all of those things are already happening, and are feeding a growing sense that what was once widely considered as ‘normal’ might actually be over.

Figure 2: Percentage of households in segments with flat or falling income, 2005-2014, in 25 advanced economies worldwide. Between 65% and 70% of households were in income segments whose average incomes stagnated or declined between 2005 and 2014, vs. 2% in the 12 years leading up to 2005. Source: McKinsey Global Institute, July 2016.

Across the world, political and economic leaders seem to be increasingly at the mercy of economic and geopolitical forces that are largely beyond their control, almost all of which can be traced back, directly or indirectly, to the stalling of the economic growth engine. These forces are feeding a seemingly unstoppable rise of economic and political instability. In developing and emerging economies, this is typically leading to power struggles, a rise of authoritarian rule, or even the outright implosion of the established order. In the industrialized world, this is leading to a phenomenon of ‘sophisticated state failure’, whereby political institutions maintain a semblance of functionality but are increasingly incapable, in the absence of genuine economic growth, of solving the major issues facing complex societies.

This evolution is feeding a rise of anger and resentment amongst citizens, which is increasingly undermining the liberal world order that prevailed in recent decades, and even in some countries the foundations of liberal democracy itself. This is arguably visible in the U.S., as shown by the ‘surprising’ result of the 2016 presidential election, as well as in Europe, which is becoming the epicenter of global geopolitical risk and where fears of a disintegration of the European Union (EU) are mounting, especially in the wake of the British citizens’ vote in favor of an exit from the bloc (‘Brexit’) in June 2016.

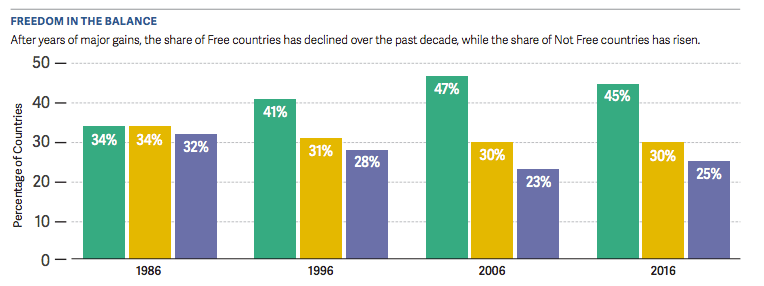

Figure 3: Share of ‘Free countries’, ‘Partly free countries’, and ‘Not free countries’, 1986-2016. A total of 67 countries suffered net declines in political rights and civil liberties in 2016, compared with 36 that registered gains. This marked the 11th consecutive year in which declines outnumbered improvements. Free countries – countries with established democracies – accounted for a larger share of the countries with declines that at any time in the past decade, and nearly one-quarter of the countries registering declines in 2016 were in Europe. Source: Freedom in the World 2017, Freedom House, January 2017.

For policy makers and for civil society, there is therefore no more important and pressing need than to understand the causes and consequences of the global dearth of economic growth, as well as the policy options that may – or may not – be available to address them.

Economists are divided on the causes and even the significance of the global dearth of growth. Many tend to interpret it through the lenses of their respective schools of thought, i.e. as resulting mostly from excessive, supply-stifling government intervention for economic liberals, or on the contrary from insufficient demand-boosting government action for the various schools of thought rooted in the ideas of John Maynard Keynes (1883-1946). A growing number of them, however, recognize that the dearth of growth might reflect something deeper.

Some economists explain that economies are structurally facing lower ‘speed limits’ – or ‘potential output growth’ – after the financial crisis – and largely because of it. They sometimes use the term ‘hysteresis’ to designate the long-lasting effects of the crisis, which they say has left persistent scars on the economic tissue and shifted the economy down to a lower expansion path. Many however acknowledge that slow economic growth is not just an after-effect of the Great Recession but part of a longer-term deceleration that predates, and indeed may have contributed to cause the financial crisis. Over the last few years they have come up with elaborate narratives to explain this economic malaise, such as the ‘secular stagnation’ narrative, which sees the cause of slow growth in either demand deficiency – i.e. in a chronic shortfall of demand resulting from population aging and the rise of income and wealth inequality – or in slower growth in potential output from the supply side – caused in particular by the diminishing returns of technological innovation. Others state that economic growth is primarily hampered by a ‘debt overhang’ – i.e. a state of excessive, generalized indebtedness of economic agents, public and/or private – and/or by the deflationary effects of the debt deleveraging process. Others still blame low growth on the process of ‘financialization’ of the economy, i.e. the expansion of a ‘parasitic’, extractive and predatory financial sector – aided according to some by misguided government and central bank policies.

These various narratives differ in focus and emphasis, but they all probably have some degree of validity and can be seen as various ways of examining a same situation from different perspectives. None of them, however, is sufficient to explain why economic growth is slowly getting extinguished at the global level and why the economic policies conducted in the last few years have, everywhere, largely failed to trigger a genuine, self-sustaining return to economic expansion.

In fact, these narratives tend to focus on developments that, even if they act as mutually reinforcing drags on growth, are symptoms of the world’s economic malaise rather than its deeper root causes. The chronic shortfall of demand, the decline of productivity growth, the relentless pile up of debt and the seemingly unstoppable financialization of the economy can all be seen as the various symptoms or consequences of a deeper and more fundamental erosion of the world economy’s capacity to expand. This erosion results from a set of developments that largely slip under the radar of most economists, who thus remain largely puzzled by the economy’s failure to pick up. As a result, the economics profession is becoming increasingly troubled and polarized, at a time when its influence on public policy has never been so strong.

Even more than from what most economists usually look at, i.e. constraints on capital and labor and on the productivity of their use, the slowdown of global economic growth since before the financial crisis might in fact be resulting from factors that they typically ignore or dismiss, i.e. constraints on the supply of energy and other biophysical resources that feed into the economic process and impact its functioning. In fact, the world’s capacity to create additional wealth is getting increasingly eroded by biophysical boundaries that over time tend to raise the acquisition costs, constrain the quantity and degrade the quality of the flows of energy and natural resources that can be delivered to the economic process, as well as by the constantly increasing costs of some of the side effects of the economic process (i.e. ‘negative externalities’ including environmental degradation such as climate change), and the growing need to ‘internalize’ them into the price system (e.g. through taxation, regulation, or subsidies).

A growing body of research shows that the following fundamental trends have played a key role in driving economic growth since the beginning of the Industrial Revolution:

- the increasing availability of cheap and high quality forms of energy inputs, and the rising efficiency of their conversion to useful or productive work;

- the increasing availability of ‘surplus energy’ (i.e. energy available to do other things than procuring, processing and distributing energy) obtained from high ‘net energy’ resources (i.e. fossil fuels, and most particularly oil);

- the increasing capacity for producers and consumers to ‘externalize’ the environmental costs of the economic process (in terms of degradation of the natural environment and depletion of natural resources) to society at large, to the ecosystems used as waste ‘sinks’, to other countries, or to future generations.

It appears, however, that these trends might have stopped and even started to reverse in recent decades.

In fact, once cheap and abundant forms of energy inputs – in particular oil, the ‘lifeblood’ of the global economy – now tend to become scarcer. The global production of ‘conventional’ oil – i.e. oil produced using drilling technologies that utilize the natural pressure of an underground reservoir – has reached a peak in 2011. The whole increase in oil production since then has been due to the growing extraction, in particular in North America, of ‘unconventional’ oil – i.e. liquid sources including oil sands, tight (shale) oil, extra heavy and offshore deepwater oil, gas to liquids and other liquids. The extraction of unconventional oil requires additional pressure and tends to be significantly more expensive, more complex, more energy intensive, and more polluting than that of conventional oil. Unconventional oil also requires more processing prior to refining to create value-added products, and is therefore less valuable in global markets. Oil industries and governments across the globe are however investing in unconventional oil sources due to the increasing scarcity of conventional oil reserves. Many of our global conventional oil supplies have indeed already been extracted, limiting the availability of these sources for future extraction.

Figure 4: World conventional and unconventional liquids production. Total production of conventional oil reached a peak in January 2011 at 86.2 mmbpd. The production of unconventional then rose sharply, before contracting following the oil price drop from $115 per barrel in June 2014 to under $35 at the end of February 2016. Total production of conventional and unconventional oil reached a peak in August 2015 at 96.9 mmbpd, which has not yet been surpassed. Source: Art Berman. Data from EIA, Drilling Info, Statistics Canada and Labyrinth Consulting Services, Inc.

Figure 5: World conventional and unconventional liquids production, with split OPEC/non-OPEC for conventional oil. Non-OPEC conventional production peaked in November 2010 at 49.8 mmbpd and has been declining since. Source: Art Berman. Data from EIA, Drilling Info, Statistics Canada and Labyrinth Consulting Services, Inc.

Figure 6: Crude oil production costs of various oil resources. As the world’s demand for oil rises, costlier resources need to be tapped, which raises average production costs globally. Source: Morgan Stanley, 2014

Figure 7: Trends in world exploration and production capital expenditures (E&P Capex) per barrel of oil. CAGR is for ‘Compound Annual Growth Rate’. The cost of worldwide oil exploration and production has been rising at a rapid rate since the turn of the 21st century. Source: Steve Kopits, based on IEA and Barclays Research data.

The depletion of conventional oil resources does not only constrain the production growth of crude oil and push up its average procurement cost worldwide, it also results in a degradation of the quality of those very energy resources that power the world’s economy. One way of measuring the quality of energy resources and their evolution is through exergy analysis, i.e. the analysis of the amounts of usable energy in a system, which is equal to the total of the free energies (e.g. kinetic, thermal, potential) in the system relative to its surrounding environment, and of its transformation though various processes (mechanical, chemical, biological, electrical) into useful work (heat, electricity, motive drive, muscle work). Even though macro-level exergy analyses are rare, recent studies suggest that most advanced economies may have already reached ‘peak exergy’ efficiency, i.e. the growth of their energy system’s exergy efficiency (as measured by their useful work output/exergy input ratio) has slowed significantly in the last decades and is well below the reported growth of their energy efficiency (as measured by their energy output/energy input ratio). This smaller rate of improvement signals a decreasing quality of energy resources and a weakening capacity of the energy supply to power productive work, which may be a significant contributor to the ‘mysterious’ slowdown of productivity growth in recent years.

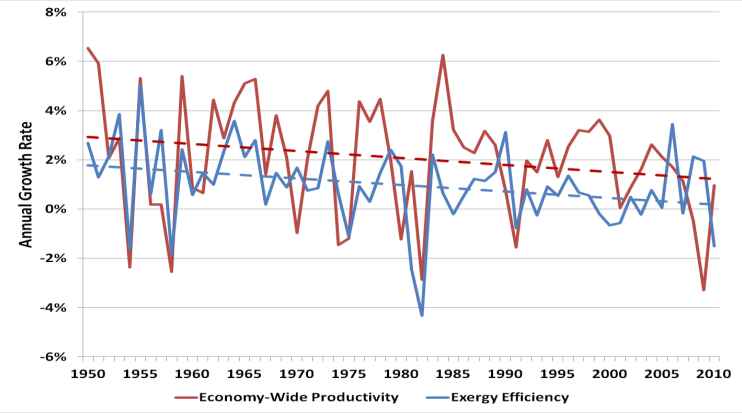

Figure 8: Growth rates for exergy efficiency and economy-wide productivity, U.S., 1950-2010. The two solid lines are the actual year-to-year change in exergy efficiency (in blue) and the economy-wide productivity (red). The dashed lines suggest the best fit trend lines, again for exergy efficiency in blue and for economy-wide productivity in red. The graph shows a tightly linked, declining trend for both exergy efficiency and productivity. Source: Linking energy efficiency to economic productivity, by John A. “Skip” Laitner, Amercian Council for an Energy-Efficient Economy, July 2013.

Another effect of the depletion of conventional oil resources is that the amount of ‘surplus energy’ delivered to the economy (i.e. amount of energy that can effectively be used for doing other things than finding, extracting, processing, converting, transporting and distributing energy) is getting increasingly constrained. The net energy gain of conventional fossil fuels indeed tends to decrease over time as resources get depleted, decrease in quality and get more difficult to obtain. Meanwhile, alternatives such as unconventional fossil fuels (e.g. shale/tight oil and gas), nuclear, bio-fuels or renewable energy sources tend to have lower net energy ratios, as measured by their EROI (energy return on investment).

Figure 9: Estimates of EROI values and trends for global publicly traded oil and gas. The analysis shows that EROI has declined by nearly 50% in the last decade and a half. New technology and production methods (deep water and horizontal drilling) help to maintain production but appear insufficient to counter the decline in EROI of conventional oil and gas. Source: Hall et al 2013, based on data from Gagnon et al 2009.

Even if the energy returns of energy sources for which long-term data may be lacking (e.g. modern renewables such as solar and wind power) is difficult to assess and may evolve in non-linear ways, the overall surplus energy tends to go down as societies and economies transition away from high net energy resources such as conventional fossil fuels and towards lower net energy resources such as unconventional fossil fuels or renewables, either voluntarily (e.g. to fight climate change) or due to resource constraints. A rising share of the total energy supply thus has to be dedicated to finding, harnessing, transforming and conveying energy to meet a growing demand, while the share that can be made available for other uses (i.e. the net to society) tends to decrease, constraining ‘discretionary’ investments and consumption. This relative decrease of surplus energy appears to be only partly offset by technology-enabled efficiency gains, and the supply of energy available for doing other things than getting energy is thus becoming increasingly constrained over time, which erodes potential economic growth at the global level.

Official data from the International Energy Agency (IEA) actually suggests that an overall downward trend of ‘surplus energy’ at global level is already underway. The share of the world’s Total Primary Energy Supply (TPES) used by the energy supply sector (which comprises all energy extraction, conversion, storage, transmission, and distribution processes that deliver final energy to end users) indeed expanded from 23% in 1973 to 33% in 2012. The share available for Total Final Consumption (TFC) by other sectors of the economy, on the other hand, went down from 76% in 1973 to 69% in 2014. Overall, the quantity of energy supplied to end-use sectors (industry, transport, buildings – including residential and services – and other – including agriculture and non-energy use) rose by 102% over the period, but the quantity of energy that had to be used to supply this energy to end users increased by 197% (data source: IEA, Key World Energy Statistics, 2016). This may reflect a relative decrease of the global average efficiency of energy conversion, transmission, and distribution systems and processes (e.g. as a result of increasing electrification of energy distribution and consumption), but it also probably signals a decrease in the net energy yield obtained from the world’s energy resources as a whole.

Furthermore, evidence also abounds that the capacity to ‘externalize’ the environmental costs of the economic process is decreasing. Confronted with the growing costs and damages of resource depletion and environmental degradation, societies tend to develop mechanisms and rules aimed at ‘internalizing’ these costs into the economic process, i.e. at imposing them, at least partially, on producers and/or consumers. This internationalization, through regulation or taxation, tends to reduce the profitability of the production process and therefore to weigh on potential economic growth. According to some estimates, none of the world’s top industries would actually be profitable if they had to pay the ‘true’ cost of the ‘natural capital’ they use, i.e. if the full costs of their environmental damage and unsustainable natural resource use were accounted for.

These various biophysical constraints, as they increase, tend to weigh more and more on the economy’s productive capacity, thus eroding the potential for productivity and output growth. Over the last decades, the industrialized world has found a workaround to those biophysical constraints by expanding the reach of global capitalism but also and maybe more fundamentally by substituting debt accumulation to genuine wealth creation. This debt-fueled growth system hit a wall in 2008-2009 and has since then only been maintained on life support by the massive monetary injections made by the world’s major central banks, as well as by the massive and compounding asset bubbles that have been blown as a result in developed as well as emerging economies. This monetary largesse has so far prevented a brutal deflation of the financial assets that underpin the entire global financial and economic system, but the ability of central bankers to contain this deflationary spiral is dwindling as time passes and as genuine growth continues to be lacking.

The root causes of the long-term erosion of the world economy’s growth potential, therefore, may be related to biophysical constraints rather than to factors affecting just capital and labour inputs. As a consequence, policies aimed at boosting or reviving economic growth by targeting solely capital and labor inputs and the productivity of their use are highly unlikely – and, as a matter of fact, have failed in recent years – to deliver their intended results. Pursuing such policies would typically mostly lead to putting ever-growing pressure on those factors of production – and most particularly on the traditionally weaker factor of production, i.e. labor – to try to obtain productivity improvements and output growth that would consistently fail to materialize. In fact, continuous dual pressure on labor – upward on productivity, downward on compensation – has already been at play for several years, and this dual pressure is a major contributor to the ‘populist’ backlash now underway in many countries.

As increasing biophysical constraints tend to weigh more and more on the economy’s productive capacity, efforts now made at boosting economic growth tend to yield diminishing returns – i.e. meaning that more and more has to be invested or ‘sacrificed’ to obtain less and less growth in return – and whatever growth is achieved comes with rising costs – financial costs in terms of rising debt, social costs in terms of rising inequality, or environmental costs in terms of environmental degradation including climate change.

To make sense of this increasingly intractable global economic malaise, policy makers worldwide struggle to find convincing answers in mainstream economic theories. Several key rules of the economics textbook seem to no longer apply, and the policies that economists from various schools of thought advocate consistently fail to deliver their intended results. Unless they start taking into account biophysical realities and constraints and how they impact the functioning of the economy, economic policies will not only continue to fail but will also inevitably stack more problems – economic, social, political and environmental – into the future. A biophysical reading of the economic process is required to make sense of the global economy’s situation and make better informed policy decisions, based on a sophisticated understanding of the underlying systems and that acknowledge the associated constraints as well as uncertainties.