China-Germany: the rise of a global manufacturing duopoly

China has now become Germany’s largest trading partner, a logical step reflecting the increasing hold of the two countries over the world’s manufacturing capability.

François-Xavier Chevallerau | March 7, 2017

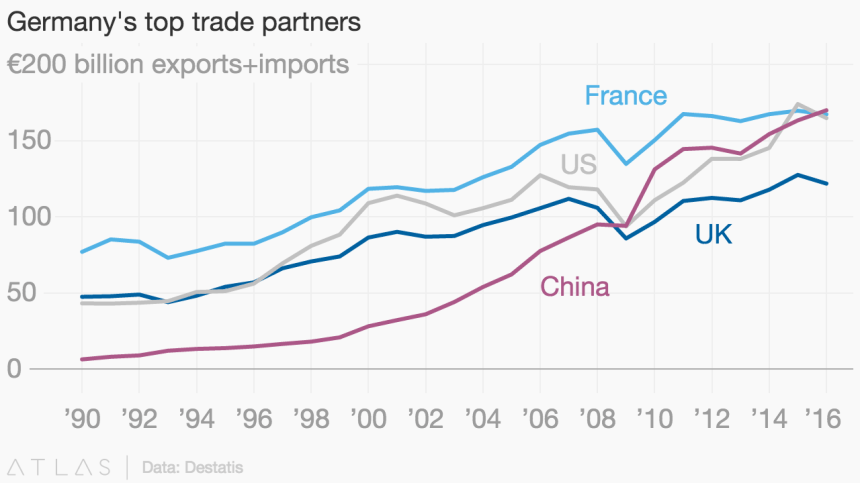

China became Germany’s largest trading partner for the first time in 2016, knocking off the United States from the top spot it briefly held in 2015. According to Germany’s Federal Statistical Office DESTATIS, the country’s imports from and exports to China rose to 170 billion euros ($180 billion) in 2016, surpassing the trade volumes of 167 billion euros between Germany and France and 165 billion euros between Germany and the U.S.

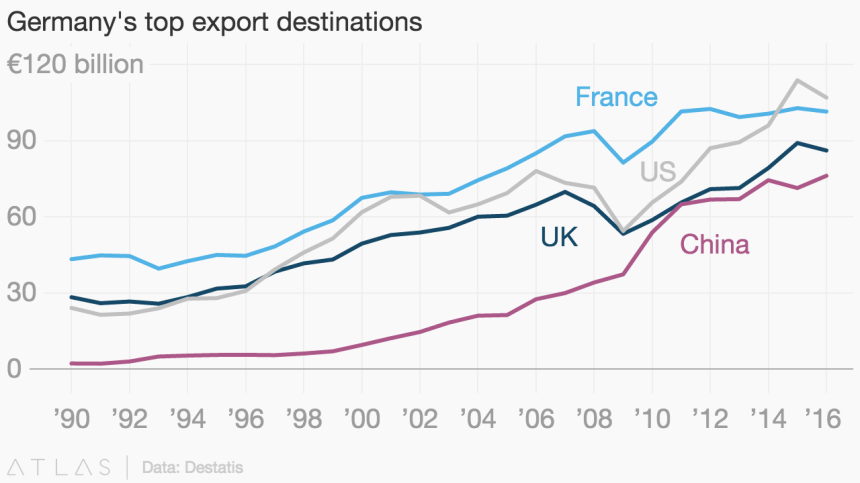

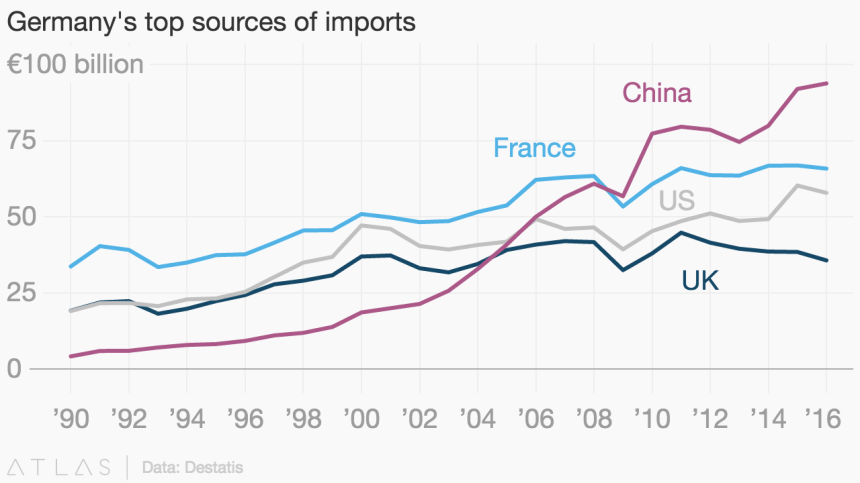

China was Germany’s fourth largest trading partner in 2015 behind the U.S., France and the Netherlands, with a combined trade volume of a little over 163 billion euros. In 2016 the U.S. remains Germany’s top export destination, and has a $65 billion trade deficit with Europe’s largest and most powerful economy. China on the other hand has been Germany’s biggest source of imports for the past eight years, and looks likely to stay in top spot for a long time to come. China’s ascendency in Germany’s trade also reflects Germany’s increasing shift away from its low-growth European partners. France had been Germany’s long-term main trade partner from 1975 to 2014.

A number of pundits were quick to explain the U.S. relegation to third spot in the trade rankings with Germany as resulting from the isolationist/protectionist stance of the new U.S. administration. However, the rise of Sino-German trade probably reflects a much deeper evolution of the patterns of global trade.

Germany and China are indeed the world’s top manufacturing powerhouses, and the world’s top exporters of goods and services – of goods much more than services, that is. They have by far the highest trade and current account surpluses ($297 billion current account surplus for Germany and $245 billion for China in 2016, according to Ifo Institute). The growing trade between the two countries reflects the increasing complementarities between their industries in the globalized economy.

For a number of reasons, Germany and China have indeed become the most competitive places where to process energy and matter to produce manufactured goods for the whole world – China specializing in mass production of low to medium value items that flood the world’s markets and Germany in higher value-added products, advanced technologies and capital goods that are very valuable to Chinese manufacturers. By doing so they have managed to capture an increasingly dominant share of the world’s manufacturing capacity and value added, while largely avoiding head-to-head competition so far. The result is the rise of a global manufacturing ‘duopoly’, which is becoming increasingly dominant as it becomes more integrated.

Despite much talk of a ‘rebalancing’ of a Chinese economy towards services and internal consumption, China remains the world’s largest manufacturer, accounting for nearly a quarter of global value added in this sector and grabbing a rising share of global trade. Germany on the other hand is the only Western European country where the share of manufacturing hasn’t decreased over the last couple of decades (source: World Bank). The close integration of its neighbors’ manufacturing capacities with its own value chains and the persistence of a favorable exchange rate have enabled the country to build a formidable export machine and to accumulate record trade surpluses in recent years, in particular over its European partners. Germany’s current account surplus is expected to have risen to 8.6% of its annual economic output in 2016, versus 8.3% in 2015. The EU sees a maximum figure of 6% as sustainable in the long term.

The massive current account surpluses of both China and Germany are largely due to trade in goods, reflecting the strength of their manufacturing base. The two countries’ success at grabbing a growing share of the world’s manufacturing value added and at deriving massive surpluses from their exports of manufactured goods seems to confirm that manufacturing remains the main source of what was once called ‘surplus value‘. The debate about the relative merits of manufacturing and services in generating wealth, productivity and economic growth is not new, but the strengthening of the China-Germany manufacturing axis, and their ever growing trade surpluses over service-oriented economies puts it under the spotlight again. “Services clearly create wealth“, The Economist’s ‘Buttonwood’ columnist noted last year, but “one wonders whether an ever-smaller manufacturing sector supporting an ever-larger services sector can generate sufficient growth“. China and Germany, obviously, have made up their minds about that a long time ago.

The end of the honeymoon between China and Germany has already been announced by some, and it is actually possible that the relations between the two countries may sour in the future if China moves into the markets for high-tech, innovative, cutting-edge manufactured goods currently dominated by Germany, including luxury cars, pharmaceuticals, or high-tech manufacturing equipment. For now, though, the world’s manufacturing duopoly keeps strengthening its grip.

Thankk you for sharing this

LikeLike